Nick Hodge,

Publisher

July 7, 2026

This week, I’ll be presenting at the Rule Symposium to an audience of more than 2,000 sophisticated investors.

I’m not going there to tell them gold matters.

They already know that.

I’m not going there to tell them copper, uranium, antimony, or critical minerals are important.

They know that too.

This is the Rule Symposium. The people in that room already understand resource cycles, capital scarcity, discoveries, and the kind of speculation that can turn a tiny company into a market darling.

What I’m going there to talk about is something different.

I’m going to talk about how serious investors actually get positioned before the broader market shows up.

And that usually does not happen by chasing a stock after the news is out.

It happens through private placements.

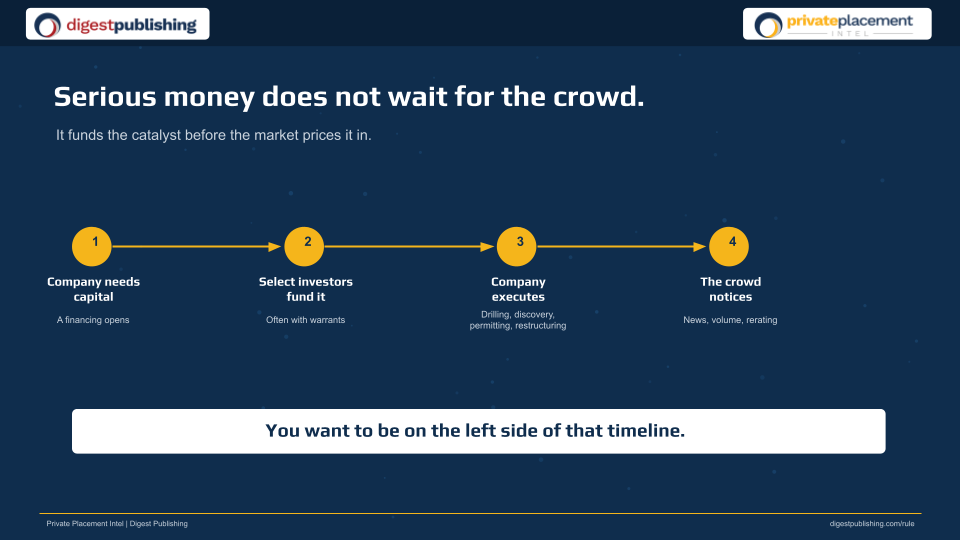

That is where a small group of qualified investors funds the catalyst before the crowd has a chance to price it in.

A company needs capital. A financing opens. A select group funds it.

The company drills, develops, acquires, permits, restructures, or goes public.

Then the market notices.

Most investors live on the right side of that timeline.

They wait for the news. They wait for volume. They wait for promotion. They wait until the chart already looks good.

Private placement investors are trying to get positioned on the left side.

That is the edge.

And it is the single biggest reason private placements have become one of the most important wealth-building tools in my career.

Every private placement I do gets a folder.

That might sound boring, but it matters.

Inside those folders are subscription documents, warrant certificates, correspondence, notes, corporate filings, hold-period dates, and the original thesis behind each deal.

Each folder represents a decision.

Sometimes it becomes dead paper. Sometimes it becomes a modest win.

Every so often, it becomes the kind of deal that changes a portfolio forever.

The best example we’ve ever had is still Patriot Battery Metals, now PMET.

We financed that company at C$0.16.

It later traded as high as C$17.80.

That was an 11,025% peak move from the financing price.

I am not telling you everyone sold the top. Nobody does that perfectly.

The point is not that the stock went up.

The point is that the setup existed before the crowd knew what it was looking at.

And the common shares were only half the story.

That financing also came with full warrants at C$0.25.

That is why structure matters.

The same discovery, with a different structure, can create a dramatically different outcome.

That is why serious investors care about warrants.

A private placement is not just buying stock.

It is a direct financing between a company and a select group of qualified investors.

You are not buying from another shareholder in the open market.

You are putting capital into the treasury.

Often, you get a better valuation.

Often, you get a warrant.

And most importantly, you are funding the work that can create the next headline instead of buying after everyone else sees it.

The edge is real. So is the risk.

But when you combine the right people, the right paper, the right project, the right price, and the right path to liquidity, the risk/reward can change dramatically.

That is what we underwrite at Private Placement Intel.

People. Paper. Project. Price. Path.

A good private placement is not just about the story.

It is about where you sit in the capital structure before the story becomes obvious.

Around last year’s Rule Symposium, we participated in a Kincora Copper (TSX-V: KCC) financing alongside serious resource investors, including Rick Rule and Jeff Phillips.

That matters because it shows the table we are trying to get closer to.

The table where experienced resource investors are not chasing the catalyst after the fact.

They are funding it.

Kincora had the ingredients we like to see: a tiny restructuring-stage valuation, tier-one porphyry districts, partner-funded exploration, technical credibility, and a full warrant.

We financed at C$0.30.

The shares have since been trading around the C$0.80–C$0.90 range.

The common shares alone have been up over 200%.

But again, the structure matters.

That financing also came with a full warrant at C$0.50 for three years.

Entry. Warrant. Catalyst. Rerating.

That is the private placement edge in practice.

And it’s not one cherry-picked example.

In the current open Private Placement Intel portfolio, we have seen major wins across different commodities, different jurisdictions, and different stages.

Q2 Metals is up 2,236.0%.

Hannan Metals is up 590.0%.

Kingsmen Resources is up 332.0%.

Daura Gold is up 283.3%.

North Shore Uranium is up 280.0%.

Kincora Copper is up 176.7%.

Vizsla Copper is up 112.0%.

Different stories. Same framework.

We are trying to fund catalysts before broader market attention arrives.

Sometimes that catalyst is a drill program. Sometimes it’s a resource. Sometimes it’s a restructuring. Or a public listing. Or a new strategic partner.

The common thread is simple:

You come in early. You may get a discount. You often get warrants.

And you fund the catalyst before the crowd shows up.

That is how serious investors access deals before the broader market.

And that is exactly why I want to talk to you about what we are doing next.

Because our newest Private Placement Intel opportunity is not a gold deal.

It is not a copper deal. It is not uranium. It is not antimony.

It is something we do not see very often.

A pre-IPO space infrastructure deal.

I am not going to name the company here.

That is reserved for Private Placement Intel members.

But I will tell you the setup.

This is a small company in the in-space logistics market.

It does not launch rockets. It doesn’t build satellites.

It’s focused on what happens after launch.

That’s important because launch is no longer the only bottleneck.

Getting to space has become cheaper, faster, and more competitive.

Satellites are multiplying. Commercial space stations are being planned.

Governments are treating space as a strategic domain.

Private capital is funding rockets, lunar landers, space tugs, orbital manufacturing, Earth observation, communications, and space infrastructure.

But if space becomes a real economy, something else has to exist.

Cargo has to move. Payloads have to be tested. Hardware has to be serviced. Stations have to be resupplied. Technologies have to be validated before they go to orbit.

And eventually, platforms in space will need the equivalent of logistics, trucking, servicing, towing, storage, and repair.

That’s the opportunity.

This company is trying to become part of that infrastructure layer.

The long-term vision is orbital logistics.

The near-term wedge is more practical: helping customers test and validate hardware in space-like environments before it goes fully to orbit.

That matters.

Because before a radiation shielding plate, sensor, battery, solar array, robotics component, communications system, defense payload, or university experiment goes into orbit, someone has to help package it, integrate it, test it, fly it, collect data, and qualify it.

That is the near-term business.

The blue sky is in-space logistics.

The company is early. The risks are high.

This is not a normal resource stock where one drill hole can validate the thesis next month.

It is a venture-style deal.

There is execution risk, financing risk, technology risk, regulatory risk, customer-conversion risk, and public-listing risk.

But this is also exactly the kind of situation Private Placement Intel exists to evaluate.

An early-stage company. A large addressable market. A clear path to a public listing. A financing structure we can understand.

And a chance to get positioned before the broader public market has a chance to price the opportunity.

The current financing is priced at C$0.80.

Each unit comes with one share and one-half warrant.

Each full warrant is exercisable at C$1.50 for two years.

The company is expected to go public through a shell transaction.

The valuation is tiny compared to better-known private space logistics companies that have recently raised money at multi-billion-dollar valuations.

In one of the hottest speculative sectors in the market.

This is the kind of deal we want our Private Placement Intel members to see before everyone else.

That’s the whole point of Private Placement Intel.

We are not trying to bring members every deal.

We are trying to bring them the deals we are willing to vet for ourselves.

The full company name, financing terms, ticker path, write-up, risk assessment, and instructions for participating are available only to members of Private Placement Intel.

Private Placement Intel is built for high-net-worth and qualified investors who want access to the same kinds of private, pre-IPO, going-public, and already-public financings that Gerardo and I review for ourselves.

Membership is limited because the financings are limited.

There are only so many allocations to go around.

And this space deal is moving now.

Click here to secure your Private Placement Intel membership before this pre-IPO space opportunity closes.

Call it like you see it,

Nick Hodge

Publisher, Bizarro World