Chris Curl,

Editor

May 14, 2026

When I first started pounding the table on Intel (NASDAQ: INTC) under 20 dollars, a lot of people thought it was quaint at best and delusional at worst.

In fact, people laughed at me.

Intel, they said, was the tired old warhorse that had missed mobile, bungled manufacturing, and ceded the AI throne to Nvidia (NASDAQ: NVDA) and friends.

My editorial from March 2025 was a contrarian bet that the market was mispricing what a retooled Intel could become.

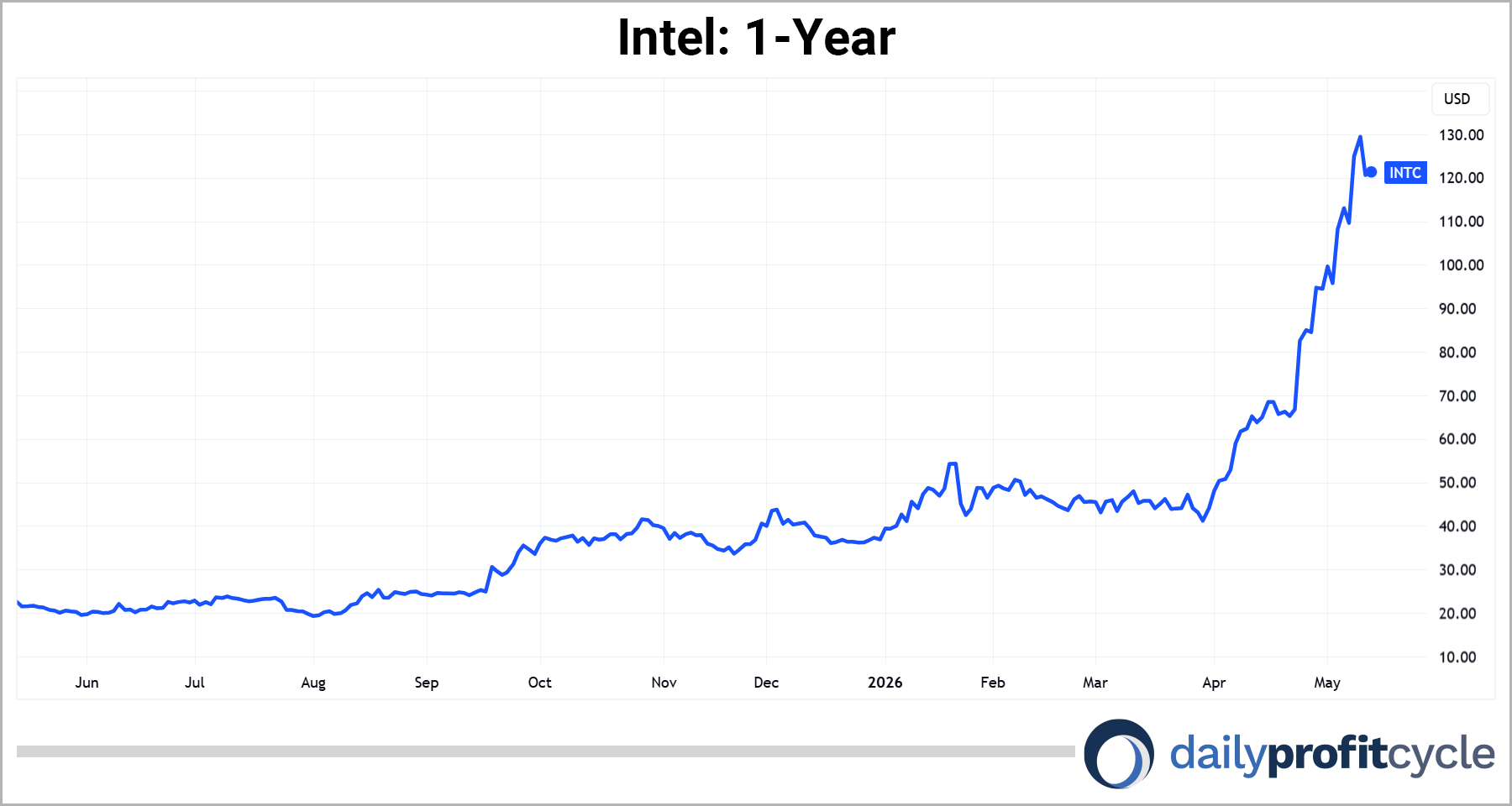

Fast‑forward a year, and the scorecard is pretty clear: Intel didn’t just survive, it ripped.

What I saw before the crowd

Back then, the narrative was simple and bearish: “Intel is late to AI, too slow, too bureaucratic.”

The stock had been left for dead while Nvidia and AMD soaked up all the AI glory. But inside Digital Dispatch, I wasn’t buying the obituary. I was looking at a different set of facts:

- A new CEO, Lip‑Bu Tan, stepped in with a mandate to restructure around AI, manufacturing, and a cleaner management hierarchy.

- A once‑in‑a‑generation capital expenditure wave backed by the CHIPS Act, the Stargate Project, and tens of billions earmarked for new fabs in Arizona, Ohio, and Oregon.

- A simple but powerful geopolitical reality: if America wants sovereign control over advanced chip manufacturing, it does not have the luxury of letting Intel fail.

That’s why I was willing to step in when Intel was trading under 20 bucks. I was not buying a perfect AI champion; I was buying a battered strategic asset with massive government tailwinds, a new playbook, and a valuation that assumed permanent mediocrity.

How the story flipped

Since then, Intel has done something the skeptics swore it couldn’t: it started to execute.

The market, which once treated Intel like a legacy value trap, has been forced to re‑rate the whole story. As AI server demand exploded, hyperscalers and enterprises realized they did not want a single‑vendor future.

Intel’s roadmap suddenly mattered again… for data‑center CPUs, for AI accelerators, for networking, and for a foundry business that could give Western governments an alternative to relying on Asia for the most critical industrial input of the 21st century.

The result: Intel’s stock is no longer languishing in the teens.

It has surged to levels that, according to recent coverage, are on track to eclipse even its dot‑com era peak, powered by stronger‑than‑expected AI‑driven revenue forecasts and renewed investor confidence. For anyone who accumulated sub $20, this is exactly the kind of asymmetry I was aiming for… double and triple‑digit percentage gains on a name the crowd had written off.

Why this is a Digital Dispatch trade, not a lucky guess

It’s tempting to chalk this up to “one good call,” but that misses the point. The Intel move is a case study in the Digital Dispatch process:

- I look for strategic chokepoints… places where technology, policy, and national interest intersect. Intel was (and is) one of them.

- I focus on narrative dislocations… moments when the story on TV (“Intel is finished”) diverges from the incentives of governments, customers, and insiders (“we need Intel to win”).

- I use macro and micro together… pairing big‑picture themes like AI sovereignty and reshoring with company‑level catalysts like leadership changes, capex cycles, and balance‑sheet support.

When you line those elements up, the risk/reward on Intel under $20 stopped looking like “catching a falling knife” and started looking like “getting paid to wait for the market to notice a structural shift.”

That’s what I do in Digital Dispatch: not chasing yesterday’s AI darlings at 20 times sales but hunting for the next misunderstood linchpins the cycle still hasn’t fully priced in.

Aging well, but what’s next?

That March 2025 article was prescient for a number of reasons. It flagged:

- The importance of Intel’s AI roadmap and the 2027 window to deliver competitive chips.

- The massive, government‑backed fab build‑out as a foundation for a manufacturing renaissance.

- The idea that Intel might be “the only viable hope America has to lead in the global manufacturing of microprocessors.”

A year later, those aren’t hypothetical talking points but the backbone of why the stock has rerated so hard. Intel’s AI bet is a core part of how investors are thinking about the entire AI hardware stack.

And here’s the important part: this is just one position from a broader Digital Dispatch playbook that spans AI, robotics, and what we’ve called the Nvidia “Atlas” moment: the buildout of the physical and digital infrastructure that will run the next economy.

If you liked what buying Intel under $20 did for your portfolio, you should be asking a simple question:

What are the current Intels (today’s hated, doubted, or misunderstood linchpins) that the market will look back on in a year or two and say, “How did we not see that coming?”

That’s where I’m spending my time now: not victory‑lapping Intel (as satisfying as that is), but applying the same framework to the next wave of AI fabs, robotics platforms, and “picks and shovels” for the embodied AI boom.

If you want to see those ideas before they look obvious on a one‑year chart, that’s exactly what Digital Dispatch is built to deliver.

Click here to get started.

Keep coming back,

Chris Curl

Editor, Bizarro World